Covered Call Blog

How to use covered calls to generate recurring income.

Most Recent

Most Popular

By Topic

By Symbol

Receive new blog articles automatically by following us:

![]() Email newsletter

Email newsletter

![]() X

X

![]() Facebook

Facebook

![]() YouTube

YouTube

![]() LinkedIn

LinkedIn

Do you have an idea for a topic you'd like us to write about? Please contact us.

ACG's Index Option Writing Study

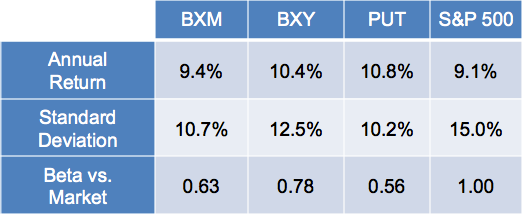

Asset Consulting Group has released an analysis of 23 years of index option writing. The results show that writing covered calls (and their equivalent, naked puts) increases returns and lowers portfolio volatility.

Two Flavors Of BuyWrite Index and Two Other Similar Indices

The ACG study looked at 4 indices that sell options for income:

- BXM - CBOE S&P 500 BuyWrite Index

writes 1-month ATM (at the money) covered calls on S&P 500 - BXY - CBOE S&P 500 2% OTM BuyWrite Index

writes 1-month 2% OTM (out of the money) covered calls on S&P 500 - PUT - CBOE S&P 500 PutWrite Index

holds T-bills and writes 1-month ATM naked puts on S&P 500 - CLL - CBOE S&P 500 95-110 Collar Index

writes 1-month 110% covered calls and buys 3-month 95% puts

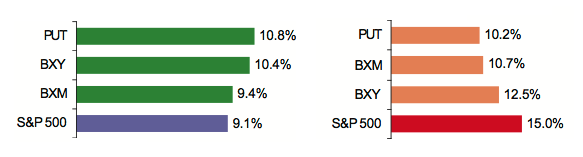

Their summary findings show that the first 3 outperformed the S&P 500 with higher annual return and lower volatility. (The CLL (collar) index actually did worse than the BuyWrite Index and PutWrite Index so we will leave it out of this discussion.)

Shown graphically with annual return on the left in green (more is better) and standard deviation on the right in peach (less is better):

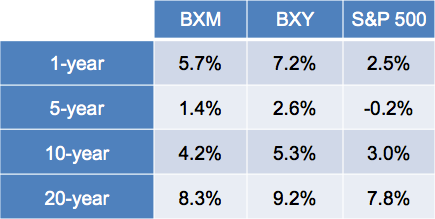

If we look at different time periods the BXM and BXY beat the S&P 500's annual return for a variety of durations (with period ending Dec 31, 2011):

For even more data, download the complete Asset Consulting Group analysis and report.

Mike Scanlin is the founder of Born To Sell and has been writing covered calls for a long time.