Covered Call Blog

How to use covered calls to generate recurring income.

Most Recent

Most Popular

By Topic

By Symbol

Receive new blog articles automatically by following us:

![]() Email newsletter

Email newsletter

![]() X

X

![]() Facebook

Facebook

![]() YouTube

YouTube

![]() LinkedIn

LinkedIn

Do you have an idea for a topic you'd like us to write about? Please contact us.

Goldman Sachs Likes Covered Index Writing

After an analysis of 15 years of buy-write index call writing, Goldman Sachs found that the strategy of writing covered calls on the S&P 500, when compared to simply buying and holding the S&P 500, increased returns and lowered portfolio volatility (similar results to several other covered call studies).

BXM is the CBOE S&P 500 BuyWrite Index. It is an index value calculated by using a strategy of writing 1-month at-the-money (ATM) covered calls on the S&P 500.

Specifically, on the third Friday of each month (option expiration day) the BXM goes long the S&P 500 and sells a 1-month ATM call option on the S&P 500. The BXM methodology assumes that this European-style call option will be sold at a price equal to the volume-weighted average of the prices of the option from 11:30am to 12pm EST.

The option is held until expiration one month later, when the strategy rolls and new near-term ATM call options are sold against the long S&P 500 holding. The option premium and any dividends on the S&P 500 constituents are assumed to be reinvested in the covered call strategy (i.e. the BXM is a total-return index).

BXM is not a tradable security, although there are a couple of ETFs that mimic it (albeit with 0.75% expense ratios), including (1) PowerShares S&P 500 ButWrite Portfolio ETF (PBP) and (2) iPath CBOE S&P 500 BuyWrite Index exchange-traded note (BWV).

Summary Results

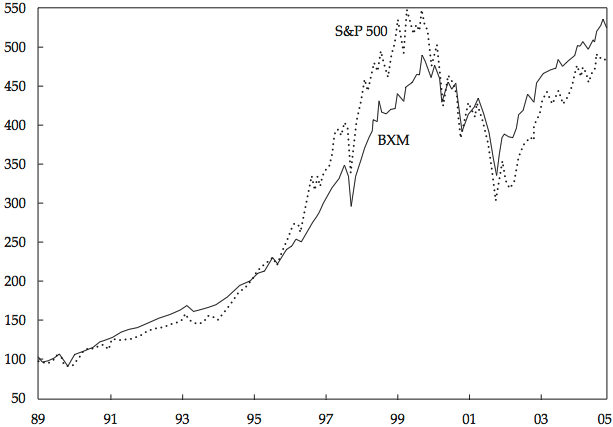

Cumulative total return on the BXM and S&P 500 from Jan 1990 to Oct 2005 shows that during a fast rising market (1995-1999) the S&P does better than BXM, but over the entire 15 year period (many market types) the BXM does better:

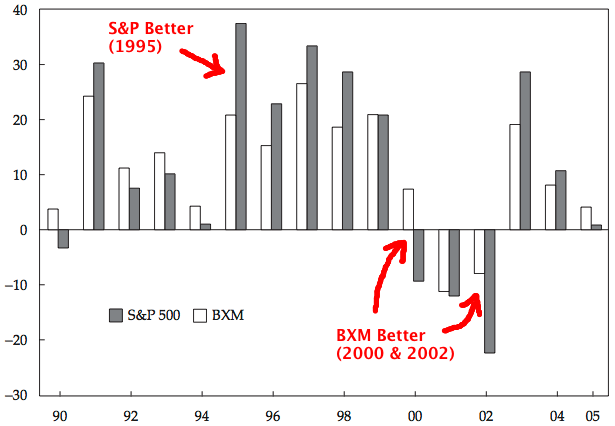

The annual returns below show a similar story: During good years the S&P outperforms (eg. 1995) but during bad years (eg. 2000 and 2002) the BXM outperforms:

Alternatives To BXM

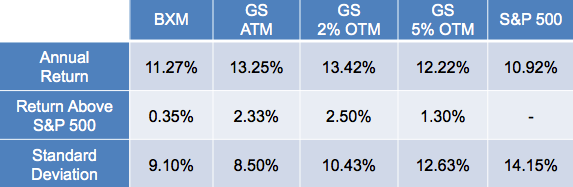

Goldman compared 3 alternative strategies to the BXM. They chose an ATM strategy (with differences to the BXM), a 2% OTM (out of the money), and a 5% OTM strategy.

The differences between Goldman's ATM strategy and the BXM's ATM strategy:

- Goldman rolled at the close on Thursday before expiration instead of Friday

- Goldman priced exact ATM calls instead of nearest to the money

- Goldman kept all of the call premium in cash instead of reinvesting it

The results show that all 4 of the index call writing strategies beat the S&P 500 and had lower volatility (smaller standard deviation) for the period 1990-2005:

Goldman's report has additional charts and figures. To see all the data, download the complete Goldman Sachs' Finding Alpha via Covered Index Writing report (46 pages).

Mike Scanlin is the founder of Born To Sell and has been writing covered calls for a long time.